Risk management is important and it needs to be part of your farming business planning. If you were unable to work in your business, due to an illness or as a result of a farming accident, the question is: Would you be able to manage your everyday living expenses or maintain your business operations?

We all know of someone who has been impacted by a farming accident, and the emotional and physical distress associated with it are clear. However, the long-term financial repercussions of an accident or illness are often less understood, and they can be devastating for the business too.

What you need to know

It’s vital to have plans in place to protect yourself and the continuity of your business. You won’t have time to think in the event of an emergency or serious medical diagnosis, so having plans already in place is crucial.

Talking about the what if’s is a particularly important element of risk management for farming families. Determining risk factors facing your business up front and enacting risk mitigation strategies, whether it be sharing the risk through insurance or avoiding the risk through good planning, will be far easier and more effective, than scrambling for solutions should you find yourself in the thick of an emergency.

Key risk management considerations should include:

Personal and business protection

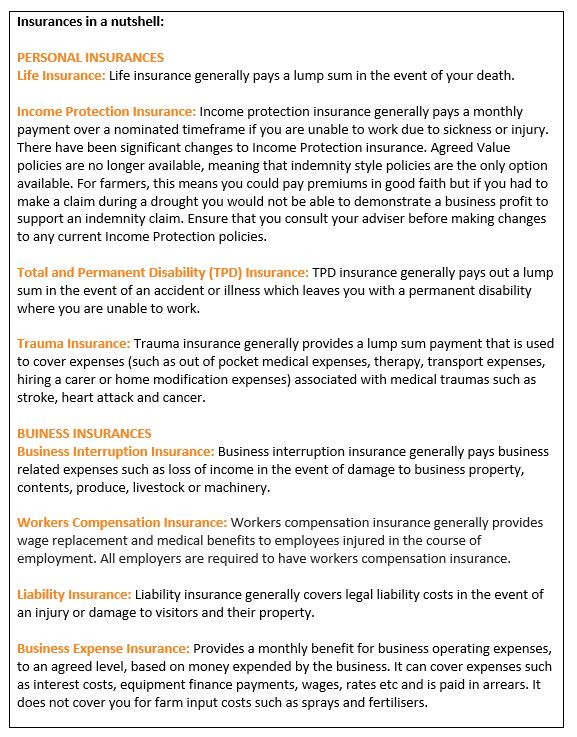

Adequate levels of insurance, both business and personal, should be central to your risk management approach.

It really is a case of horses for courses, ensuring the protection measures you put in place are specific to the needs of your particular farming business and you personally.

Considerations that will include whether you pay yourself a wage or take drawings from the business; and your cash flow will need to be taken into account when choosing the personal protection policy that’s right for you.

It’s important to know whether or not your business insurance extends to operating costs, your personal drawings and crop input costs. You also need to be aware that, generally, claims on your insurance are paid in arrears, which may also impact your cash flow needs.

If you employ staff, they must be covered by workers compensation, it is imperative to have all your paperwork and systems in order to ensure you can prove you are addressing your responsibilities.

Without appropriate mechanisms in place, a Worker’s Compensation claim could result in years of legal proceedings AND emotional and financial consequences.

Risk management is more complex for farming families and farm businesses so it is likely you will need professional help to implement protection strategies that are suitable for your individual situation.

GRDC have some helpful risk management resources including this Farm Business Risk fact sheet and the Risk Management section of the Farming the Business Manual.

Succession Planning

Succession planning is crucial for protecting the needs of your family and working towards a successful handover for the family business. Taking a structured approach and considering the needs of all family members is vital. Finding the right balance of negotiations and compromise for your family is the key. You will need advice from a number of professionals who have specialised succession planning knowledge and who will understand the complex needs of individual family members as well as the importance of achieving positive outcomes for the business from a tax, legal and cash flow perspective. Read more in our Five Steps for Succession Success series of articles.

Business continuity planning

You need to consider how your business could keep operating if you were not there to manage it. This may involve: Outlining potential risks and vulnerabilities for the business, including considering the implications if key people were unable to work, including yourself; Considering the what-if’s such as paying someone else to manage the business when you can’t; or reducing outputs in the short-term or other compromises to accommodate certain events.

You will also need to identify clear roles and responsibilities, then share your plan with your team and those in your extended business networks who will be vital in dealing with unforeseen events.

Establishing regular toolbox meetings can also be an effective way of sharing knowledge and involving others in identifying risks, priorities, required maintenance activities, as well as financial and seasonal stress triggers. Ideally, your goal would be to test different scenarios, set the short-term direction to be able to share the load so you are prepared in the event of an emergency and you are unable to work for a period of time.

How we can help

With a career that spans more than 30 years, Dibbo has a deep understanding of the challenges experienced by rural families. He is well-qualified to provide rural advice and agribusiness solutions including risk management, financial planning, mortgage broking and business consulting services. Dibbo also has a special interest in developing and implementing practical and achievable succession plans.

We know first-hand the importance of contingency planning, read our personal story.

If you would like to discuss your overall risk management needs, including your business and personal protection needs, I encourage you to contact me today on 08 8253 2906 or email info@financialservicessa.com.au

Phillip Dibben is a financial adviser at Active Financial Management. Active Financial Management and its advisers are Authorised Representatives of Fortnum Private Wealth Ltd ABN 54 139 889 535 AFSL 357306.

Phillip Dibben is also an Authorised Credit Representative of Riverland Lending Services Pty Ltd, ABN 37 145 814 080 ACL 391825

This information does not consider your personal circumstances (including taxation) and is of a general nature only. You should not act on the information provided without first obtaining advice specific to your circumstances.