Achieving tax efficiencies and making the most of your personal or business cashflow is all part of well-considered financial planning. However, you’ll need to plan ahead of tax time.

Whether you are a young family, the owner of a business or farming enterprise or heading into your retirement years, there are financial planning strategies involving tax efficiencies you should consider.

A little bit of planning in the lead up to the end of financial year will help you to know where you stand so you have time to make any necessary adjustments to your affairs to benefit your financial position.

End of financial year strategies

- Review your cashflow position

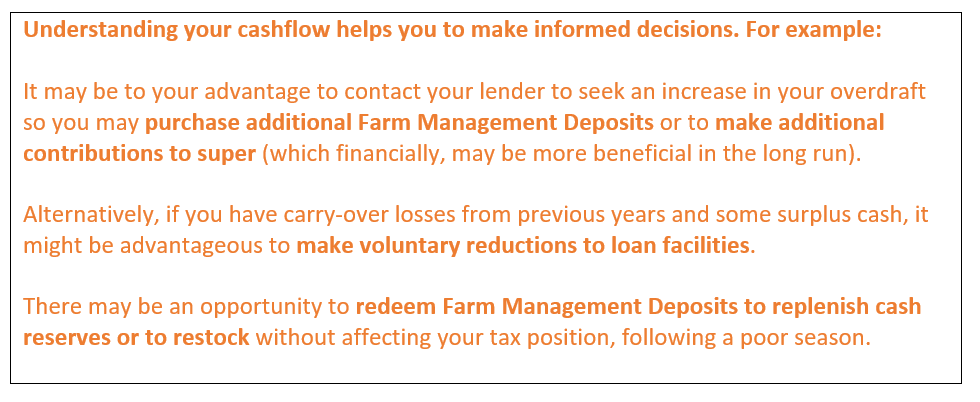

Mapping out your cash flow until the end of financial year enables you to initiate strategies that will assist you in meeting your goals, and help determine your year-end tax position.

- Boost your super

You can boost your super balance through pre-tax (concessional) super contributions. You are allowed to make up to $25,000 in pre-tax contributions each financial year (which also includes salary sacrifice arrangements). Concessional contributions are taxed at 15%.

You could also consider building your super balance with after-tax (non-concessional) contributions with an allowance of up to $100,000 in each financial year or up to $300,000 using the bring-forward rule for balances less than $1.4 million.

- Know the rules associated with super to avoid penalties

If you have paid yourself or any employee wages this financial year, you are obligated to pay Superannuation Guarantee contributions of 9.5%. You will also need to consider the time required by clearing houses to transfer funds into employee super funds before June 30.

If you have a SMSF and your fund is paying a pension to members, minimum pension payments must be made (and received by the member) before June 30 to avoid penalties.

- Pre-pay or plan tax deductible expenses or income

You may be able to pre-pay expenses such as an investment loan or some personal insurances, to bring forward deductible expenses which can help to reduce your taxable income this financial year. Alternatively, it may be beneficial to defer income from grain, wool or livestock until after the end of the financial year to assist with tax management.

Don’t go it alone

Prioritising your affairs to consider your short- and long-term financial goals can be complicated, so it’s important to seek professional assistance. Working collaboratively with your accountant, financial adviser and business adviser can help you make more informed decision making in consideration of your complete financial and business needs. Indeed, it is our experience that collaboration is key for achieving tax efficiencies, optimal cash flow for business operations and the peace of mind that your business and personal affairs are in order.

Don’t leave your end of financial year planning until the last minute. Planning is key to meeting your short term and long-term financial goals. Assume the financial year ends in May and work to have all year end jobs done by that time rather than rushing to try and beat deadlines. Please contact me today on 08 8253 2906 or email info@financialservicessa.com.au to discuss how we can help you.

Phillip Dibben is a financial adviser at Active Financial Management. Active Financial Management and its advisers are Authorised Representatives of Fortnum Private Wealth Ltd ABN 54 139 889 535 AFSL 357306 trading as Fortnum Financial Advisers.

This information does not consider your personal circumstances (including taxation) and is of a general nature only. You should not act on the information provided without first obtaining advice specific to your circumstances.