If you have put your super planning ‘out to pasture’ due to the competing demands on excess cash associated with running a family farming business, your super balance may not be in tip-top shape.

But making contributions to super just got a whole lot easier… You can now ‘carry-forward’ unused pre-tax contribution amounts from 1 July 2018, allowing you to catch-up your unused super contributions for up to five years. Coupled with the existing rule allowing you to ‘bring forward’ your after-tax contributions to super, you now have real opportunity to boost your super to build your savings for your retirement.

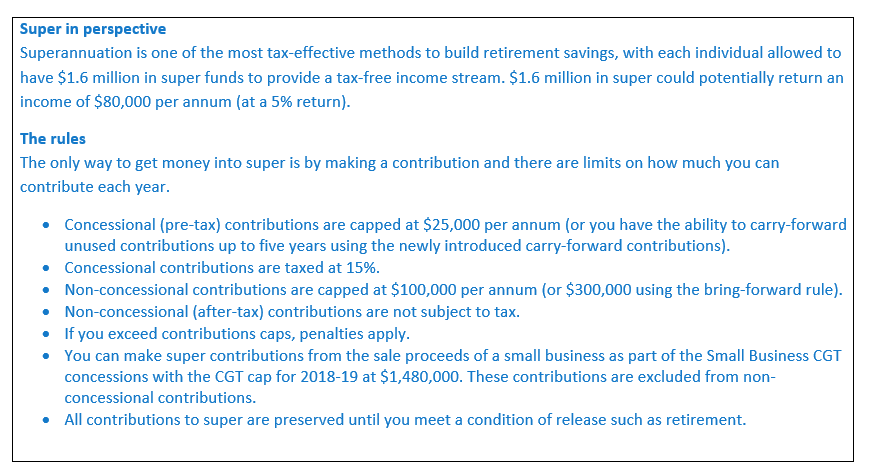

Super is one of the most tax-effective ways to build your retirement savings. Similar to Farm Management Deposits (FMD), which enable you to set aside tax-deductible deposits when your business is thriving for use in the leaner years, the ‘carry forward’ and ‘bring forward’ strategies can help you boost your super balance during your more prosperous years.

Pre-tax contributions to super: How do carry-forward contributions work?

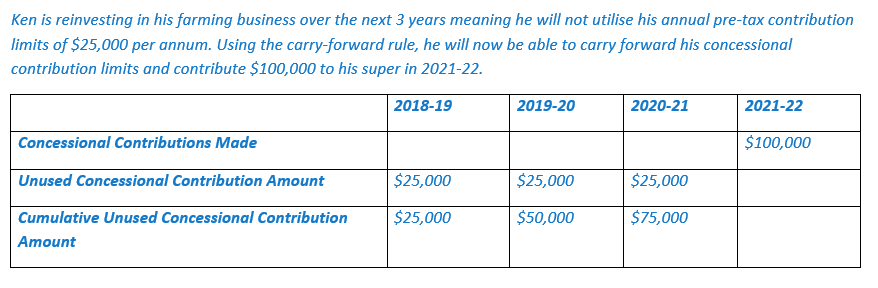

Carry forward contributions help you to take advantage of unused concessional (pre-tax) contribution caps by carrying forward any unused contribution allowances over a five year period. The concessional contribution cap is $25,000 per annum.

Due to fluctuations in cashflow associated with seasonal factors, many farmers are not in a position to utilise annual concessional (pre-tax) contribution limits each year, so this new rule may be beneficial for boosting your super. The scenario below explains how:

The carry-forward contributions rule is especially beneficial for business owners or those who work part-time. Carry-forward contributions only apply to people under 65 years of age who have a super balance less than $500,000. Concessional contributions include employer Super Guarantee contributions and salary sacrifice contributions.

After-tax contributions to super: How does the bring-forward rule work?

Annual limits for after-tax (non-concessional) contributions are capped at $100,000 per year. The bring-forward rule enables you to bring forward three years of non-concessional contributions and contribute up to $300,000 in one financial year to your super.

The bring-forward rule can be a useful strategy for farmers, close to retirement, wishing to capitalise on a good season.

You can only utilise the full benefit of the bring-forward-rule if you are less than 65 and have less than $1.4 million in super (further restrictions apply for balances between $1.4 and $1.5 million). Non-concessional contributions are not subject to tax, however if you exceed the annual cap, the excess amount will be taxed at 47%.

Retirement planning for farming families – getting the balance right

Decisions about contributing to superannuation come down to personal choice, competing cashflow requirements and your individual financial and retirement goals. It’s important to seek professional financial advice to help you consider your superannuation strategy with reference to your overall financial obligations, goals and objectives.

We recommend meeting with your accountant and financial planner each April to review your financial planning considerations, FMD deposits and tax liabilities prior to the end of the financial year. It’s important to note that once you retire and ultimately stop farming operations, the full amount of your FMD will be considered as part of your taxable income for that financial year.

Your superannuation strategy should be considered in the context of your retirement plans and as part of your overall succession planning. At Active Financial Management, we have a personal interest in helping family farming businesses implement practical solutions to help them make the most of their personal and business situation, including strategies to fund your retirement. Dibbo has been helping primary producers and family business owners in rural and remote locations for more than 30 years.

If you would like to discuss your superannuation strategy or retirement planning needs, I encourage you to contact me today on 08 8253 2906 or email info@financialservicessa.com.au to arrange an appointment.

Our article A balancing act – super planning for farming families provides further information about super strategies for farming families.

Phillip Dibben is a financial adviser with Active Financial Management. Active Financial Management and its advisers are Authorised Representatives of Fortnum Private Wealth Ltd ABN 54 139 889 535 AFSL 357306.

This information does not consider your personal circumstances (including taxation) and is of a general nature only. You should not act on the information provided without first obtaining advice specific to your circumstances.